The 2024 Timeline To Buying A House In The UK

The full process of buying a property has many different steps and is not a process that should ever be rushed into. All of the necessary checks must be diligently completed and the legal aspects all need to be 100% correct.

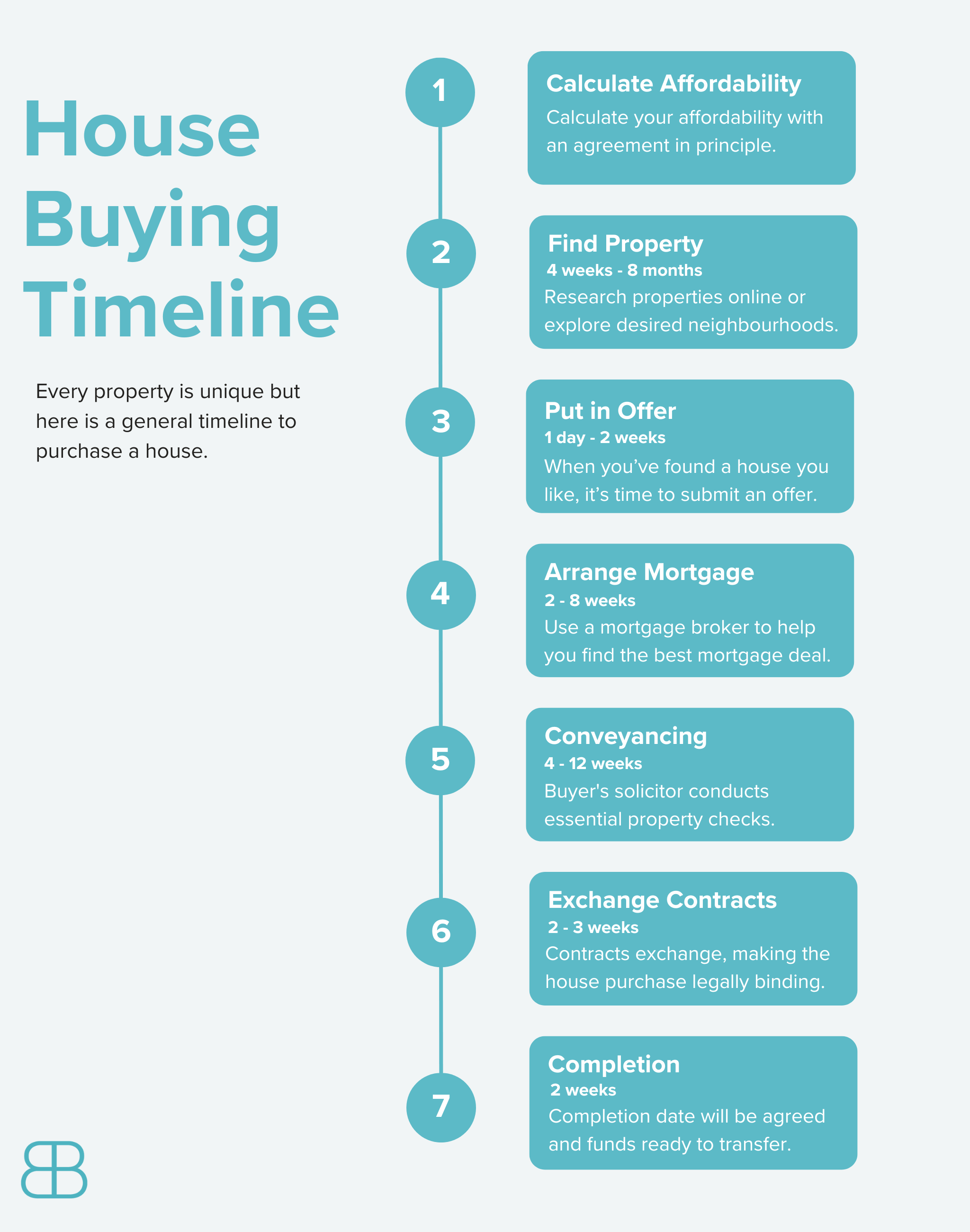

This guide takes you through the 7 step process to buying a house so you can get a better idea of the overall timeline.

Short for time? Here’s a quick video overview of the mortgage process.

- How long does it take to buy a property?

- Typical timeline for a property purchase

- Step 1: Calculating affordability - instant estimate

- Step 2: Finding a property - 4 weeks to 8 months

- Step 3: Putting in the offer and getting it accepted - 1 day to 2 weeks

- Step 4: Getting your mortgage set up - 2 to 8 weeks

- Step 5: Conveyancing - 4 to 12 weeks

- Step 6: Exchanging of contracts - 2 to 3 weeks

- Step 7: Completion - 2 weeks

- Tips to speed up the process

How long does it take to buy a property?

On average it takes around 15 weeks to purchase a house, once an offer is accepted. But every property purchase has its own unique circumstances that will determine the length of the process. There can be factors that are completely out of the homebuyer’s control, for example if the current homeowner is also in the process of buying a property this is known as a ‘chain’. In property chains, all parties must wait until the buyers and sellers are in a position to exchange contracts until they can complete on their purchases.

Free phone and video consultations are provided in the U.K.

Get StartedTypical timeline for a property purchase

Here is the usual timeframe for are each stage of the house buying process, with some actions overlapping. If everything goes smoothly, you could be in your new home within a couple of months, but delays might extend the timeline.

Step 1: Calculating affordability – instant estimate

The first step in the process is to calculate how much you can afford to spend on a property by getting an agreement in principle (AIP). If you start viewing houses that are out of your price range, this will waste a lot of time and effort. Many mortgage lenders have affordability calculators on their website, or you could use a broker to help calculate the price range of properties you should be looking for.

Remember, as well as the mortgage repayments, there will be additional costs involved in buying a property, such as a mortgage arrangement fee, solicitors’ fees and other potential costs. These costs should be factored into your affordability calculations.

Step 2: Finding a property – 4 weeks to 8 months

The time it takes to find a property depends on the availability of the type of property you are looking for. If your requirements are specific, for example, you are looking in a particular area where not many properties are going up for sale, it could take a long time. But, if you want a new build property and there are several housing developments being built in an area you are interested in, then it could be a lot quicker.

The stage of finding a property you want to buy will usually include online research using estate agents’ websites, or even driving around the area you are interested in living.

Step 3: Putting in the offer and getting it accepted – 1 day to 2 weeks

If you’ve found your perfect property, the next step is to put an offer in. When you go to view the property, you can put in an offer immediately if the estate agent is open for you to to do so. However, the property owner may not want to accept your offer, or may choose to consider it whilst other interested parties continue to view the property.

Choosing how much to offer is a difficult decision, as you run the risk of losing the property if your offer is too low but could end up paying more than needed if you put in a high offer.

It is a good idea to do some research regarding recent house sales for similar properties in the area, to give you an idea of the offers that have been accepted. You can also look at how quickly houses are being sold in the area. If they are staying on the market for a while it can indicate that there are not many offers being made and a lower offer could be accepted.

When your offer has been accepted, you are not legally bound to buy the property until the exchange of contracts, so there is a possibility that you could still get gazumped i.e. someone else comes in with a higher offer. If this happens, you go back to square one and start looking for a new property all over again.

Step 4: Getting your mortgage set up – 2 to 8 weeks

This part of the buying process is an important one and even if you are keen to get your house purchase completed quickly, finding the best mortgage deal could save you a lot of money. You should do as much research as possible in this stage or seek advice from a mortgage broker to find you the best deal based on your circumstances.

It is important to look at a range of different mortgage deals, getting comparisons that take all of the associated costs into account, including the interest rate as well as additional costs from the mortgage lender for arranging the mortgage.

Once you have found the right mortgage deal for you, it’s time to apply for your mortgage. Again, this step can vary in length depending on the specific details involved in the mortgage. The applicant’s financial situation is one factor that can add complications and the condition of the property. Or issues with the valuation can also complicate the length of the application process.

Your mortgage lender will ask for documents, such as proof of income, and will conduct credit checks before agreeing to lend to you. To speed up the process, you should have all of the required documentation ready to provide to your mortgage lender.

If there are any issues with credit history, the lender could decline your mortgage in which case you would need to find another mortgage deal. This is why many people with bad credit work with a broker to find mortgage deals tailored to their circumstances, increasing approval chances.

The mortgage lender will require a valuation of the property to make sure that they are not lending more money than the property is worth. They risk losing money if the applicant fails to keep up with the mortgage payments and the house must be repossessed and sold. The valuation is a key factor in their decision to approve the mortgage.

Within this stage of the house buying process, the mortgage applicant will usually arrange for a survey to be completed, so they can find out if there are any structural issues or other potential problems with the property. If there is a lot of work required, this report could be used to negotiate and lower the price of the property.

Alternatively, the buyer might want to pull out of the purchase altogether or get the current owner to arrange for repairs to be completed. The latter option would mean that it will take considerably longer for the house purchase to go through.

If the mortgage decision is straightforward and there are no added complications then the only hold-ups should be arranging the valuation appointment, which can be completed in around 2 weeks.

Even though you can apply for a mortgage by yourself, you should consider using a mortgage broker to process the application on your behalf. There are many brokers, such as Boon Brokers, who will not charge a client fee at any stage of the mortgage application process and can remove all the stress incurred from communicating with lenders.

See What Our Clients Have To Say

Step 5: Conveyancing – 4 to 12 weeks

You will need to select a conveyancing firm to complete the legal work on your behalf. Your mortgage lender or broker may recommend a conveyancer, or the estate agent you are buying the property through may have a solicitor that they usually work with.

Conveyancing encompasses all of the work that is completed by the buyer’s solicitor. It includes doing environmental searches and researching any planning permission issues, amongst other important checks. They basically do all of the research required to make sure that you are unlikely to face any unexpected problems further down the line once you legally own the property.

This work can be the longest part of the process and the timescales can vary. It not only depends on how busy your solicitor is, but how quickly the third party companies come back with the relevant information regarding the searches. There are a large number of searches to complete and if there are any unusual findings from the searches, this can increase the time.

Another area of work that the solicitor will be doing at this stage is drafting the land registry and contracts, which needs input from both the seller and their conveyancer. The contract can take about one month to finalise.

Step 6: Exchanging of contracts – 2 to 3 weeks

The exchanging of contracts between the buyer and the seller will usually take about 2-3 weeks. This part involves the conveyancers getting the copies signed and exchanged to make the house purchase agreement legally binding.

During this stage, the buyer will provide their solicitor with the deposit for the property, so you will need to check whether your bank has a limit on the amount of money you can move out in one day. You may need to spend several days moving money out, if your deposit amount is over the limit permitted.

Before you complete, you should have your buildings insurance ready to start from the completion date, to make sure your property is insured as soon as it legally becomes yours. You can always change the start date of the policy if there are any unexpected delays with the completion of the sale.

Step 7: Completion – 2 weeks

A completion date will be agreed and the transfer of funds from the mortgage lender will be scheduled. The agreed completion date will be determined between the buyer and the seller, trying to find a suitable date for both sides. If the seller does not have a new property to go to yet, they could push for the date to be delayed. This might suit the buyer’s circumstances but if not, negotiations will need to take place to agree on a date.

If everything goes according to plan, the buyer can collect the keys to their new home and move in on the day of the completion. The solicitor will provide them with a completion statement that outlines any outstanding payments such as stamp duty, outstanding deposit amount and their conveyancing fees.

The conveyancer will arrange for the funds to be transferred and if there is any stamp duty to be paid, the conveyancer will also arrange for the payment to be made to HMRC. The final parts of the process are then registering the new ownership with the Land Registry (which the conveyancer will take care of) and obtaining copies of the property’s new title deeds.

Tips to speed up the process

The timeline for buying a property is difficult to predict, as there are so many factors that are involved. Delays can arise from being in a chain or if there are any issues from the survey or valuation.

If you want to ensure that your property purchase goes through as smoothly and quick as possible, there are a few actions you can take to help. For example, doing more research to create a shortlist of areas/property types that you could be interested in if one falls through. It can be difficult to not feel strongly attached to one specific property but the more open-minded you stay in terms of property possibilities, the quicker you will be in your new home.

Another key factor is careful considering the services you use such as conveyancers, brokers and mortgage lenders. It is a good idea to read reviews about the different services you require, so that any big problems could potentially be highlighted.

Some mortgage lenders will have much faster application processing times than others, so if you read a few reviews that are complaining about how hard it was to get hold of the mortgage team, or how unnecessarily long the processing took, you should steer clear if you want a fast end-to-end process.

The same approach applies to the conveyancers, some are painfully slow and you will find that you end up chasing them for pretty much every action and update. If someone has recommended the conveyancer to you, then they will hopefully have confirmed that the conveyancer is very efficient and therefore won’t hold progress up.

Using a mortgage broker can really help speed up the mortgage application process. An experienced, knowledgeable broker will be able to find you the best mortgage deals for your circumstances, and do so very quickly, saving you the time and effort of searching yourself. They will also be able to tell you exactly what documents and other requirements you need to provide to the lender, which will also save you lots of time.

Boon Brokers provides transparent and professional mortgage advice without charging any fee for our services. Contact us today if you would like help finding the best mortgage deal and speed up the house buying process.

Gerard BoonB.A. (Hons), CeMAP, CeRER

Gerard is a co-founder and partner of Boon Brokers. Having studied many areas of financial services at the University of Leeds, and following completion of his CeMAP and CeRER qualifications, Gerard has acquired a vast knowledge of the mortgage, insurance and equity release industry.Related Articles

- How Long Does A Mortgage Application Take?

- What Proof Of Income Is Needed For A Mortgage?

- What Documents Are Needed For A Mortgage?

- Reasons Why Mortgage Applications Are Declined

- How Much Deposit For A Mortgage?

- Should I Use My Estate Agents Mortgage Broker?

- What Is A Guarantor Mortgage

- How To Get A £250,000 Mortgage

- What Should I Ask When Buying A House?

Authorised and regulated by the Financial Conduct Authority. No: 973757

Authorised and regulated by the Financial Conduct Authority. No: 973757